What is the Prostate Cancer Nuclear Medicine Diagnostics Market Overview – Definition, scope, and significance?

The Prostate Cancer Nuclear Medicine Diagnostics Market encompasses the development, production, and distribution of radiopharmaceuticals and imaging systems used to detect and stage prostate cancer through positron emission tomography (PET) and single‑photon emission computed tomography (SPECT). The scope includes PET products such as F‑18, C‑11, and Ga‑68‑PSMA, as well as related services delivered to hospitals and clinics worldwide. This market is significant because early and accurate diagnosis directly influences treatment decisions, improves patient outcomes, and reduces long‑term healthcare costs associated with advanced disease management.

What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising prostate cancer incidence, growing clinical acceptance of PSMA‑targeted imaging, and reimbursement reforms that favor advanced diagnostics. Restraints involve high production costs of short‑half‑life isotopes and stringent regulatory pathways. Challenges arise from limited isotope supply chains and the need for specialized imaging infrastructure. Opportunities stem from emerging theranostic combinations, expansion into emerging economies, and the development of kit‑based radiopharmaceuticals that simplify on‑site preparation.

What are the current growth trends shaping the market?

Current trends feature a shift from conventional bone scans to PSMA‑targeted PET imaging, rapid adoption of Ga‑68‑PSMA agents, and integration of artificial intelligence for image interpretation. Additionally, collaborations between diagnostic firms and pharmaceutical companies to co‑develop companion diagnostics are accelerating market momentum. The trend toward decentralized imaging in outpatient clinics is also gaining traction, supported by portable PET/SPECT solutions.

How has COVID‑19 impacted the market and what is the recovery trajectory?

The pandemic caused temporary delays in elective imaging procedures and disrupted isotope supply chains, leading to a short‑term dip in market activity. However, post‑2021, demand rebounded quickly as healthcare systems prioritized cancer diagnostics to prevent treatment delays. The recovery trajectory is now positive, with accelerated adoption of remote workflow technologies and a renewed focus on resilient supply networks, positioning the market for robust growth.

What does the competitive landscape look like and how is the market consolidating?

The competitive landscape is fragmented but increasingly consolidating through strategic alliances, mergers, and licensing deals. Major players such as Lantheus Medical Imaging, Novartis, and Telix Pharmaceuticals dominate the PET segment, while niche firms like ABX Advanced Biochemical Compounds and Blue Earth Diagnostics specialize in specific isotopes. Recent collaborations between radiopharma companies and imaging equipment manufacturers indicate a trend toward integrated solution offerings.

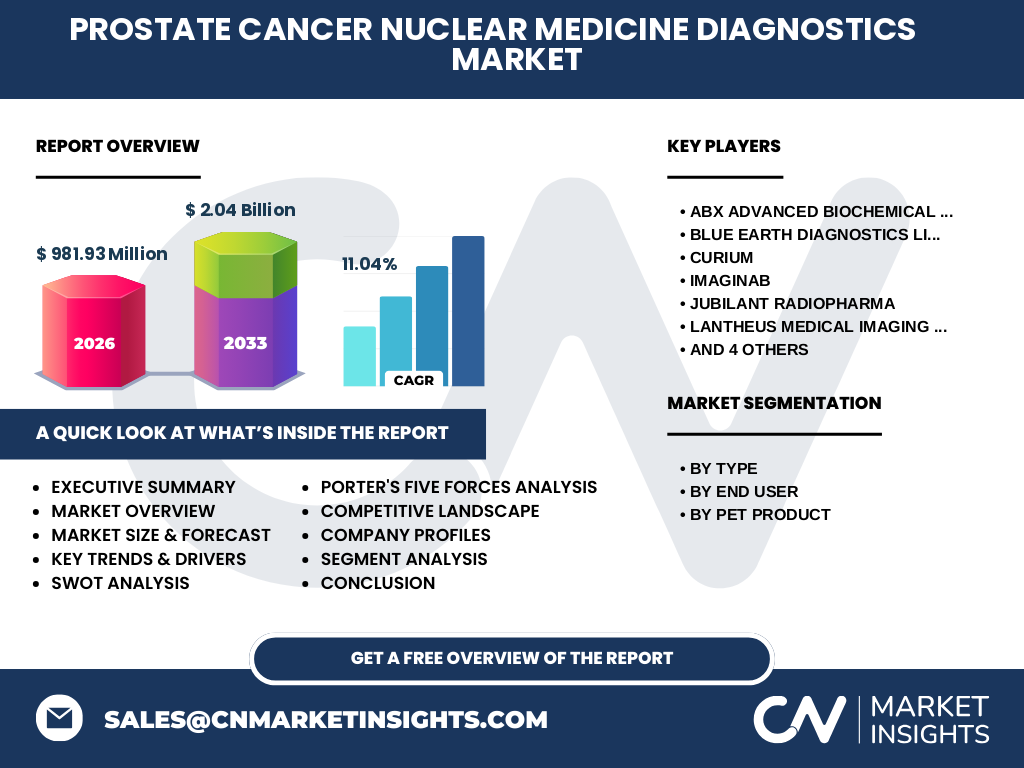

What are the key findings in the executive summary?

The market is valued at $981.93 million in 2026 and is projected to reach $2.04 billion by 2033, delivering an 11.04% CAGR. Growth is propelled by PSMA‑targeted PET imaging, expanding hospital networks, and supportive reimbursement policies. Despite supply constraints for short‑lived isotopes, innovators are addressing these gaps through kit‑based formulations and regional production hubs. Competitive dynamics favor firms that can combine radiopharmaceutical expertise with advanced imaging platforms.

What are the market forecasts for 2025‑2032?

Forecasts indicate a steady upward trajectory, with the market expected to more than double its 2026 size by 2033, reflecting the 11.04% CAGR. Year‑over‑year growth is driven by rising adoption of Ga‑68‑PSMA, increasing hospital procurement budgets, and expansion into outpatient clinics. The forecast underscores sustained demand for both PET and SPECT modalities, with PET expected to capture the larger share due to superior diagnostic accuracy.

How is the market sized and shared by segmentation?

Segmentation by type divides the market into PET and SPECT, with PET commanding the majority share owing to the clinical superiority of PSMA‑targeted agents. By end‑user, hospitals represent the largest consumption base, followed by clinics that are rapidly adopting portable PET solutions. Within PET products, Ga‑68‑PSMA shows the fastest growth, while F‑18 and C‑11 maintain steady demand for broader oncologic applications.

What is the global market size and share by region?

While precise regional figures are not disclosed, the global market reached $981.93 million in 2026 and is expected to grow to $2.04 billion by 2033. North America and Europe lead adoption due to advanced healthcare infrastructure and early reimbursement approvals. Asia‑Pacific is emerging as a high‑growth region, driven by increasing cancer screening programs and investment in diagnostic technology.

What does the regional analysis reveal about market performance?

North America benefits from strong R&D pipelines and early FDA approvals of PSMA agents, resulting in higher per‑capita utilization. Europe shows robust uptake through unified health‑technology assessments that facilitate reimbursement. Asia‑Pacific markets are expanding rapidly as governments prioritize cancer early detection, though they face challenges related to isotope importation and regulatory harmonization. Latin America and the Middle East present modest but growing demand as private healthcare expands.

Which companies are leading the market and what are their strategies?

Key companies include ABX Advanced Biochemical Compounds, Blue Earth Diagnostics, Curium, ImaginAB, Jubilant Radiopharma, Lantheus Medical Imaging, NCM‑USA, Novartis, Telix Pharmaceuticals, and Theragonostics. Strategies revolve around expanding product portfolios (e.g., Ga‑68‑PSMA kits), securing exclusive distribution rights, investing in isotope production facilities, and forming partnerships with imaging device manufacturers to deliver end‑to‑end diagnostic solutions.

How does Porter’s Five Forces assess the market?

• Threat of new entrants: Moderate, due to high capital and regulatory barriers. • Bargaining power of suppliers: High, because few providers control raw isotopes. • Bargaining power of buyers: Growing, as hospitals demand cost‑effective kits and volume discounts. • Threat of substitutes: Low, since nuclear imaging remains the gold standard for molecular prostate cancer detection. • Competitive rivalry: Intense, driven by innovation, licensing deals, and geographic expansion.

What are the SWOT insights for the market?

Strengths: Proven clinical efficacy of PSMA PET, strong reimbursement trends. Weaknesses: Limited isotope shelf‑life and supply chain fragility. Opportunities: Development of kit‑based radiopharmaceuticals, entry into emerging markets, and theranostic pairings. Threats: Regulatory delays, potential competition from alternative imaging modalities such as MRI‑ultrasound fusion techniques.

What does the value chain analysis reveal?

The value chain starts with isotope production (cyclotrons, generators), followed by radiopharmaceutical synthesis, quality control, and packaging. Next comes distribution to hospitals and clinics, where imaging devices (PET/SPECT scanners) conduct the diagnostic procedure. Post‑scan, data interpretation services and reporting complete the chain. Value is created primarily at the synthesis and imaging stages, where differentiation through higher specific activity and faster kit preparation adds competitive advantage.

What are the key investment insights?

Investors should prioritize companies with vertically integrated isotope production to mitigate supply risk, and firms that have secured regulatory approval for Ga‑68‑PSMA kits, as these are positioned for rapid market capture. Strategic investments in AI‑enhanced image analysis platforms and partnerships that bundle radiopharmaceuticals with imaging equipment can generate synergistic returns. Emerging market entrants offering cost‑effective solutions also present attractive upside potential.

What conclusions can be drawn from the market analysis?

The Prostate Cancer Nuclear Medicine Diagnostics Market is on a strong growth path, underpinned by clinical demand for PSMA‑targeted PET imaging and supportive reimbursement environments. While supply chain constraints remain a challenge, ongoing innovations in kit‑based production and regional isotope generation are likely to alleviate pressures. Companies that combine robust product pipelines with strategic collaborations will dominate the landscape through 2033.

How was the research conducted?

The study employed a mixed‑method approach, combining primary interviews with key opinion leaders, radiopharma executives, and imaging specialists, alongside secondary data extraction from industry reports, regulatory filings, and company press releases. Quantitative analysis used historical market figures and the provided CAGR to project future size, while qualitative insights were derived from trend analysis and competitive benchmarking.

What is the scope of the research?

The scope covers global market valuation, segmentation by type, end‑user, and PET product, and regional performance across major geographies. It includes analysis of the competitive landscape, value chain, and strategic factors influencing growth. The research does not extend to detailed pricing models or country‑specific regulatory timelines beyond the data supplied.

Who are the key companies and what recent developments have they announced?

Leading firms such as Lantheus Medical Imaging have launched an updated Ga‑68‑PSMA kit with improved shelf‑life. Novartis announced a partnership with a cyclotron network to secure isotope supply for its F‑18 agents. Telix Pharmaceuticals obtained FDA clearance for a novel C‑11‑based tracer aimed at earlier detection. Theragonostics entered a joint venture with a regional hospital chain to pilot point‑of‑care PET imaging in clinics. These developments signal a focus on supply security, regulatory advancement, and expanded accessibility.